Guide to P11D Form Deadlines, Penalties & How to File: Your 2026-2027 Guide

Admin

June 19, 2026

0 Comments

If you employ staff or receive benefits through your company, the P11D form is something you cannot afford to ignore. Every year, thousands of UK employers submit inaccurate returns, and HMRC has no hesitation in handing out penalties as a result.

Whether you are a small business owner, a company director, or a payroll manager juggling multiple employees, this guide breaks down everything you need to know about P11D benefits, key deadlines, how penalties work, and the step-by-step process for getting your submission right in 2026/27.

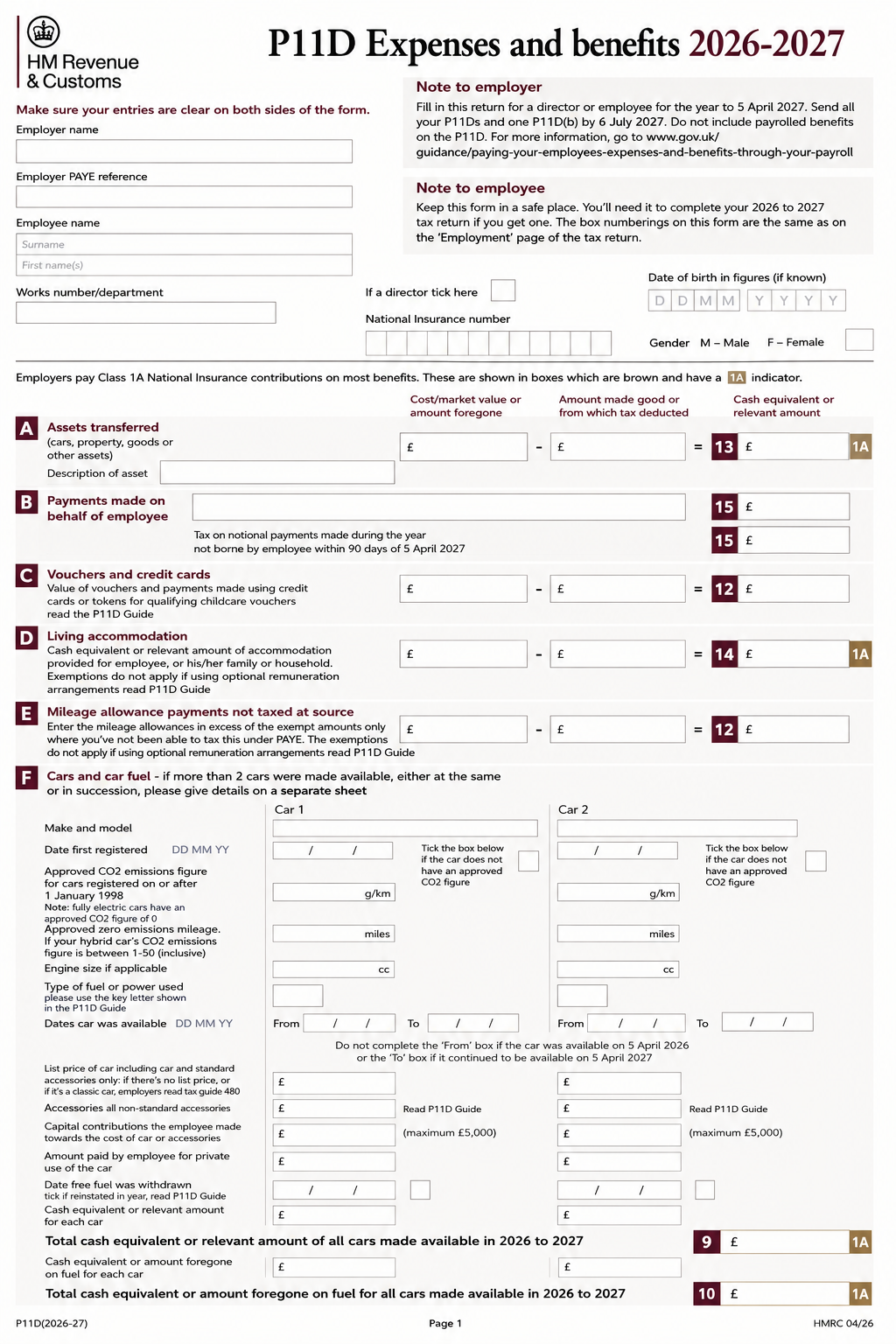

The P11D form is an official HMRC document used by employers to declare the value of non-cash benefits and expenses known as Benefits in Kind (BiK) provided to employees and directors during the tax year.

What exactly is a Benefit in Kind (BiK)?

A Benefit in Kind is any non-cash benefit or perk that an employer provides in addition to an employee’s salary or wages. These benefits often have a taxable value and must be reported to HMRC.

Common examples of Benefits in Kind include the following:

- Company cars

- Private medical insurance

- Low-interest or interest-free loans (beneficial loans)

- Employer-provided accommodation

- Assets gifted or transferred to employees

- Certain business travel, entertainment, and expense-related benefits

Employers are responsible for accurately reporting these benefits, typically through a P11D form, to ensure compliance with HMRC requirements.

The P11D meaning extends beyond a simple reporting exercise. Because Benefits in Kind have a monetary value, they are treated as a form of income by HMRC. That means they attract Income Tax for the employee and, in most cases, Class 1A National Insurance Contributions (NICs) for the employer. The P11D form ensures the correct amounts are captured and taxed accordingly.

P11D benefits cover a wide range of perks that employers provide in addition to salary. Not everything qualifies. HMRC draws a clear line between reportable benefits and those that fall under exemption, but the most commonly reported items include:

- Company cars and fuel – any vehicle provided for private use, including commuting

- Private medical or dental insurance – where the employer funds the policy

- Beneficial loans – loans made at a rate below HMRC's official rate of interest

- Living accommodation – property provided rent-free or at a below-market rate

- Assets transferred to employees – such as computers or furniture given for personal use

- Non-business travel and entertainment – personal expenses reimbursed by the company

It is worth noting that not all workplace benefits are reportable. HMRC exempts several common items from P11D reporting, including one employer-provided mobile phone per employee, approved business travel expenses, workplace parking, trivial benefits under £50 in value (provided they are not cash, performance-related, or contractual), and certain professional subscriptions essential to the role.

If you are unsure whether a specific benefit needs to be reported, the safest course of action is to check the HMRC guidance directly or seek advice from a tax professional.

One source of genuine confusion for many employers is the distinction between the P11D and the P11D(b).

The P11D is completed for each individual employee or director who received reportable benefits during the tax year. It records the type and taxable value of every benefit provided to that person.

The P11D(b) is a separate employer-level declaration that summarises the total Class 1A NICs owed on all benefits across the workforce. Rather than being produced per employee, a single P11D(b) covers the entire organisation.

Think of it this way: the P11D tells HMRC what each employee received; the P11D(b) tells HMRC how much the employer owes in National Insurance on the back of those benefits.

Both documents carry their own filing obligations and deadlines, so it is important not to conflate the two.

For the 2025/26 tax year (ending 5 April 2026), the following P11D deadlines apply:

6 July 2026 - P11D Submission Deadline

This is the headline date. All P11D forms for individual employees, along with the P11D(b) employer declaration, must be filed with HMRC by 6 July 2026. This is also the date by which employees must receive their own copy of the P11D or a written statement of equivalent information so that they can check their own tax position.

19 July 2026 - P11D Payment Deadline (Cheque or Postal Payment)

If you are paying the Class 1A National Insurance owed by cheque or through the post, payment must reach HMRC by 19 July 2026.

22 July 2026 - P11D Payment Deadline (Electronic Payment)

For the majority of employers who pay online, the P11D payment deadline is 22 July 2026. This is the date by which funds must clear in HMRC's account, not simply the date on which a payment is initiated, so build in sufficient time if you are transferring from a business account.

Missing any of these dates, even by a single day, can trigger penalties.

HMRC deadlines are strictly enforced, and late submissions can result in significant financial penalties.

Late Filing of P11D(b)

If your P11D(b) is filed after the 6 July deadline, HMRC will charge £100 per 50 employees for each month (or part month) that the return remains outstanding. For businesses with larger headcounts, those monthly charges accumulate rapidly.

Inaccurate Returns

Where a P11D or P11D(b) contains errors, the penalty depends on the nature of the mistake and the amount of tax or NIC that was underpaid as a result:

- Careless errors - penalties can range from 0% to 30% of the unpaid tax or NIC

- Deliberate inaccuracies - penalties of up to 70% may apply

- Deliberate and concealed errors - HMRC can charge up to 100% of the amount lost

Interest on Late Payments

In addition to filing penalties, HMRC charges interest on any Class 1A NIC paid after the relevant payment deadline. This applies regardless of whether the late payment was a mistake or an oversight, so it is important to pay on time even if your return was submitted correctly.

The message is clear: accuracy and punctuality are both essential when it comes to P11D compliance.

Since 2023, HMRC has required all P11D and P11D(b) submissions to be made digitally. Paper forms are no longer accepted, and any employer attempting to submit by post risks missing the deadline entirely without even knowing it.

Here is how to approach the filing process:

Step 1: Identify All Reportable Benefits

Review all 2025/26 benefit and expense arrangements, including company cars, insurance, loans, accommodation, and other perks, and confirm reporting requirements by cross‑referencing HMRC exemptions.

Step 2: Calculate the Taxable Value of Each Benefit

Apply HMRC rules to calculate the taxable “P11D value” for each benefit type, ensuring the correct methodology is used. For example, valuing company cars by list price, CO₂ emissions, and fuel type rather than employer cost.

Step 3: Prepare Individual P11D Forms

Complete a separate P11D for each employee or director who received reportable benefits. Ensure that the values entered are accurate, consistent with payroll records, and reflective of the full tax year period.

Step 4: Complete the P11D(b)

Total up the taxable value of all benefits across the organisation, then apply the current Class 1A NIC rate (13.8% for 2025/26) to determine the employer's NIC liability. Record this on the P11D(b) declaration.

Step 5: Choose Your Filing Method

You have three options for submitting P11D forms to HMRC:

- HMRC's online service - a free option suitable for employers with up to 500 employees, accessible via the Government Gateway

- Payroll or accounting software - platforms such as Xero, Sage, and QuickBooks allow direct submission from within the software, which reduces the risk of transcription errors

- A payroll bureau or accountant - outsourcing the process to a qualified professional ensures that calculations are correct, exemptions are applied appropriately, and deadlines are met without placing the burden on internal staff

Step 6: Provide Employee Copies

By 6 July 2026, every employee who received benefits must be given either a copy of their P11D or a written statement of equivalent benefit information. This is a legal requirement, not a courtesy, and failure to comply can itself attract penalties.

Step 7: Pay the Class 1A NIC Due

Submit payment to HMRC before the relevant deadline:

19 July if paying by post

22 July if paying electronically

Retain confirmation of payment for your records.

This is a question that has become increasingly relevant following HMRC's move to mandate the payrolling of most Benefits in Kind from 6 April 2026.

If you have correctly registered for and applied payrolling throughout the 2025/26 tax year, you do not need to submit individual P11D forms for those payrolled benefits. Tax on those perks has already been collected through PAYE in real time, so a separate year-end return is unnecessary.

However, for 2025/26, a P11D(b) is still required to account for Class 1A NIC on payrolled benefits.

From 2026/27 onwards, the landscape changes further. With mandatory payrolling now in force, Class 1A NIC will be calculated and reported through payroll in real time for most employers, which means the P11D(b) will no longer be required in the majority of cases. The main exceptions are employers who provided loans or living accommodation during the year — these benefits are excluded from mandatory payrolling and must still be reported via a P11D where applicable.

If you have not yet registered for payrolling of benefits, it is worth speaking to a payroll specialist about whether this approach makes sense for your business going forward.

If you are an employer who provided any taxable benefits or reimbursed non-exempt expenses to employees or directors during the 2025/26 tax year, you are almost certainly required to file. This includes:

- Limited companies, including those where the sole employee is also the director

- Sole traders and partnerships with employees receiving benefits

- Charities and non-profit organisations with paid staff

- Businesses of any size, from micro-enterprises to large corporates

You are not required to file if you provided no benefits at all, if every benefit was fully payrolled and exempt from individual P11D reporting, or if all benefits fell within HMRC's recognised exemptions.

When in doubt, err on the side of filing. HMRC is far more forgiving of an unnecessary nil return than of a missed submission for taxable benefits.

Even experienced payroll teams can fall into familiar traps when it comes to P11D reporting. The most common errors include:

- Overlooking director benefits - it is easy to focus on employees and forget that benefits provided to company directors must also be reported

- Applying the wrong benefit value - particularly for company cars, where the list price and emissions-based rules can trip up those unfamiliar with the methodology

- Confusing exempt and non-exempt items - not every perk qualifies for exemption, and assumptions made without checking the rules can result in under-reporting

- Missing the employee copy deadline - the obligation to provide employees with their benefit information by 6 July is often overlooked

- Failing to account for part-year benefits - if a benefit was only in place for part of the tax year, the taxable value must be apportioned accordingly

A thorough internal review before submission, ideally against a standardised P11D checklist, goes a long way towards catching these issues before they become costly.

If you are unsure whether a particular employee benefit should be reported on a P11D or qualifies for an exemption, Consultax Chartered Accountants can help. We provide expert advice on Benefits in Kind, review your employee benefit arrangements, and ensure all reporting obligations are met correctly. By identifying the most tax-efficient approach and helping you stay compliant with HMRC regulations; we can save your business valuable time, reduce risk, and help avoid costly penalties. Contact Consultax today for professional payroll and tax support tailored to your business.

Conclusion

The P11D form has long been a fixture of UK employer compliance, and whilst its role is evolving with the shift towards real-time payrolling, it remains a critical obligation for many businesses in 2026/27. Getting it right requires a clear understanding of which benefits are reportable, how to calculate their taxable value, and perhaps most importantly, when the deadlines fall.

The P11D submission deadline of 6 July, the payment deadlines of 19 and 22 July, and the obligation to provide employees with their benefit information are all non-negotiable. Miss them, and HMRC will not hesitate to issue penalties and interest charges.

If your business is navigating P11D reporting for the first time, or if payrolling changes have left you uncertain about what you still need to file, professional advice is always a worthwhile investment. The cost of getting it right upfront is invariably lower than the cost of correcting it afterwards.

Category:

Taxation

Tags:

Tax Filing, Taxation

Comments (0)

No comments yet. Be the first to comment!

Leave Comment